Parenting the Markets

Successful parenting involves subscribing to a philosophy and sticking with it. For example, if the goal is limiting screen time to play video games or bounce around on social media, you have to stick with those limits. There will be countless opportunities to stray from the goal; perhaps as a parent you are burnt out and just need the quiet time, perhaps their friends are doing it and it is “normal”. Sticking to it means not taking the easy route in the short term because you can see the long-term benefit even if your kids (or pets!) temporarily don’t like you very much.

Successful investing is no different. Over the years we have learned that our core philosophies will be under attack from time to time, but by sticking with them, we have achieved our goals. Within our core beliefs, there are several things we try our best not to do.

- Don’t watch the markets daily. This encourages noise trading which is not helpful given that the odds of being up or down on any given day is about 50-50.

- Don’t chase the latest hot stock or investment theme. This rarely ends well. Many might recall the cannabis stocks of 2017-2018.

- Don’t wait for the next pullback of X% to buy. This erodes the effects of compounding and none of us are equipped with a crystal ball.

- Don’t own a company just because it is cheap. Owning a good company at a fair price has proven to be a better proposition than owning a weak company at a cheap price.

- “All-or -nothing” approaches to investing can end in ruin. Diversification might deliver a constant state of regret relative to what the 20/20 hindsight investor expects, but it rarely ends in ruin.

By avoiding these behaviours, we are allowing the market to do its job, which is what many investors have struggled with in the past.

Source: John Boyle

Source: John Boyle

Why is it that over last 20 years, the average investor has performed so much worse than the markets? The main reason is that we let emotion drive our decisions. Trying to time the markets by getting out when things look bleak and back in when things look promising, leads to this performance gap.

What are we doing?

We have always tried to win by preparing and not reacting. Over the course of the last 12 months, we have added to areas that typically do well in an inflationary environment, we have tried to limit our bond exposure as much as we dared, and we have double and triple checked our diversification. Although these changes have helped, the negative momentum persists for the time being. We will continue to control what we can control and make changes only if the facts change. As the old saying goes; Investing is like a bar of soap, the more you handle it, the less you have.

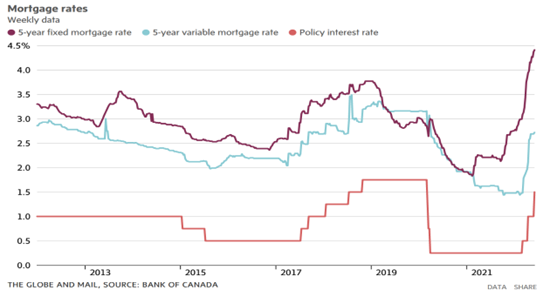

What to do with your Variable Rate Mortgage or Line of Credit?

The probability that interest rates will continue to increase throughout 2022 is high. Although we are still in the camp that the majority of the rate hikes will occur in 2022 and flatten out in 2023, it’s always good to be prepared. Our suggestion for anyone who has a variable rate mortgage or line of credit is to begin a monthly savings plan for 10% to 20% of your monthly payment. This will provide you with a pool of capital to draw from in order to meet higher monthly payments if this comes to fruition. This also gets you into the habit of having less cash flow for future months. If the higher rates don’t materialize, great, you have prepaid your next vacation!

Beware of Financial Fraud!

Attempted financial fraud is on the rise. Please be skeptical of any and every call, e-mail or advertisement that is linked to your finances. If you are suspicious, stop, and do not proceed until you have an opinion from someone else. We are happy to be a resource in this regard if needed!

8 Tips to avoid Financial Fraud